by Farlina Said and Angeline Tan, April 2024

About ISIS Malaysia

The Institute of Strategic & International Studies (ISIS) Malaysia, established on 8 April 1983 as an autonomous research organisation, focuses on foreign policy, security, economics, social policy, nation-building, technology, innovation and environmental studies.

As a premier think-tank, ISIS Malaysia engages in Track-Two diplomacy and fosters regional integration and international cooperation through networks, such as ASEAN Institutes of Strategic & International Studies (ASEAN-ISIS), Pacific Economic Cooperation Council (PECC) and Network of East Asian Think-Tanks (NEAT).

About the contributors

Farlina Said is a fellow in the Cyber and Technology Policy team in ISIS Malaysia. Her research interest includes strategic issues in cyberspace, digital development, tech governance and power dynamics in critical technologies. She has participated in forums, such as the East Asia Summit (EAS) workshops, Internet Governance Forum (IGF) open forum, Singapore International Cyber Week and platforms on the sidelines of the UN.

Angeline Tan is an analyst in the Foreign Policy and Security Studies team in ISIS Malaysia. Her research covers East Asia’s international relations with a particular focus on China. As tech rivalry escalates between US and China, she is interested in the rapidly changing landscape of the global semiconductor supply chain and how this might affect technological developments in China and Southeast Asia. She was a visiting research fellow at the Japan Institute of International Affairs (JIIA) in 2023 and has presented at the 2024 Nikkei Future of Asia Forum.

Key takeaways

- Malaysia’s immense electrical and electronics (E&E) ecosystem is the result of its industrial policies dating back to the 1970s. More than five decades later, Malaysia has development corridors catering to the semiconductor global value chain, especially in assembly, testing and packaging. The decades since the 1970s have also seen global supply chains being highly concentrated and dependent on certain companies and countries, with vulnerabilities being spotlighted following the pandemic.

- The US-China technology rivalry has added a dimension of competition, supply chain bifurcation and export controls resulting in national assessments of industrial policies weighed against national security risks and geostrategic partnerships. The rivalry will reshape the value chain, opening spaces for new players in various roles, such as Japan, India and Vietnam. Malaysia will have the opportunity move upstream vertically and horizontally where the first means entrenching and growing strengths in a subset of the supply chain. The latter refers to moving to the front-end of the value chain.

- Malaysia’s means of navigating the way forward lies in reinvigorating industrial policies and tapping into opportunities that strengthen its position in the supply chain. To do this, Malaysia must address challenges, such as customising incentives, winning talent, investing in research and development and providing clarity to ease the doing of business.

- As challenges with talent and capacity projection could reside in public messaging and branding, it may be useful to boast about Malaysia’s capabilities in the semiconductor supply chain. Growing a global player in the thriving sector could cement its position in the industry.

- Malaysia can consider deepening strengths in assembly, testing and packaging, especially to accommodate global appetite for smaller and efficient semiconductors. The advent of advanced packaging could utilise Malaysia’s strengths and matured industries in this subsector of the value chain. Much needed is capital and training should upstreaming on this front be considered.

- Lastly is the need for Malaysia to cultivate design capabilities by developing an ecosystem that could harness talent and knowledge transfers. Models of research institutes pooling resources for R&D, commercialisation and technology transfers should be considered especially in the enterprise environment.

1. Introduction

Malaysia’s electrical and electronics (E&E) sector took off in the 1970s and has seen an impressive compounded annual growth of 16% in exports over the past 50 years.1 The E&E sector remains a major driver of the economy, contributing an estimated 5.5% to the country’s GDP2 and 37% of exports in 2021.3 Today, Malaysia is the sixth largest semiconductor exporter globally4 and commands 13% of global assembly, testing and packaging (ATP).5

The semiconductor ecosystem is primarily concentrated in Penang, where facilities as well as supporting industries allow related companies to start with ease, especially due to the availability of support in parts, hi-tech machinery, equipment and well-connected logistics.6<s/up> The country’s ambitions for its semiconductor industry are guided by the New Industrial Master Plan (NIMP) 2030.7 Among the masterplan’s goals are:

- To create global IC design champions, especially to meet growing demand by new sectors, such as electric vehicle (EV), renewable energy (RE) and artificial intelligence (AI);

- To attract a global leader to establish wafer-fabrication facilities;

- To increase global share in high-tech manufacturing exports to 6%

Other goals include mentions by the deputy prime minister to grow Malaysia’s share of global semiconductor ATP activities from 13% to 15% by 2030.8

Malaysia’s recent National Semiconductor Strategy touts a living document with the following targets:

- To court at least RM500 billion investments, inclusive of domestic direct investments for IC design, advanced packaging and manufacturing equipment as well as FDI for wafer fabs and manufacturing equipment;

- To establish at least 10 Malaysian companies in design and advanced packaging with revenues between RM1 billion and RM4.7 billion and at least 100 semiconductor-related companies with revenues close to RM1 billion;

- Higher wages for Malaysian workers;

- Develop Malaysia as a global R&D hub for semiconductors;

- To train and upskill 60,000 Malaysian engineers;

- To allocate RM25 billion in fiscal support to operationalise the NSS with targeted incentives.

Despite ambitions, there are hurdles to overcome in meeting these goals. Malaysia’s semiconductor industry is impacted by recent trends (see below).

1.1 Shocks to global supply chain

The global semiconductor industry faced significant supply chain disruptions during the pandemic. In 2020, car manufacturers drastically reduced their semiconductor orders in anticipation of a market slowdown because of lockdowns and reduced travels. In response, semiconductor firms, such as Taiwan Semiconductor Manufacturing Company (TSMC), reallocated its production capacities towards high-end chips for consumer electronics, such as laptops and smartphones, which saw a surge in demand due to remote working and learning trends.

However, demand for cars grew rapidly by the end of 2020, resulting in a mismatch between surging demand and already redirected supply. Nonetheless, Malaysia’s E&E industry was able to withstand these pressures as the global supply chain was still relatively stable.

In 2021, the global semiconductor supply chain came under further strain following the cold wave in Texas and a fabrication plant fire in Japan. This resulted in production halts and consequent backlogs, with worldwide production losses estimated at US$110 billion by May 2021.9

These events coincided with Malaysia’s full movement-control order (MCO), which restricted the country’s E&E sector to operate at 60% capacity before vaccination rates picked up. This caused major production cuts in leading car makers like Toyota, Ford, General Motors and Nissan.10

1.2 US-China technology rivalry

The US-China tech rivalry is underpinned by China’s growing stature in the global arena and its techno- nationalist ambitions exemplified through policies, such as Made in China 2025. The fraying US-Sino relationship, worsened by allegations of economic espionage and national security concerns from China’s technologies in American critical systems, has encouraged Washington to hamper Beijing’s growth in advanced critical technologies. This led the US to introduce policies aimed at bifurcating and de-risking its systems, as well as where they operate.

The tech rivalry has resulted in the bifurcation of the semiconductor industry with examples of policies and efforts listed in Appendix 1. Ongoing bifurcations are frequently coupled with homeshoring efforts, such as the US CHIPS and Science Act 2022 or friendshoring between partner nations. However, the rivalry is concentrated on the design and production of advanced chips, although this definition may be subject to change.

For example, in August 2023, NVIDIA was served a letter to restrict shipments of A100 and H100 chips due to the innovation of advanced packaging or “chiplets” falling within boundaries of US export controls.11 This is a departure from the position a year earlier where the export of such chips only required a licence.12 To mitigate this, companies with a strong presence in China have shifted business plans to other types of chips, such as next-to-leading or legacy nodes, inclusive of China’s production.

Further examples of bifurcation are alliances such as Chips4 and the introduction of export controls. The Chips4 grouping – consisting of US, Japan, Taiwan and South Korea – shapes supply chains, exemplified by TSMC increasing its presence in Japan and the US. In January 2023 the US, Netherlands and Japan restricted exports of advanced chip-making machinery to China.13 In response, in July 2023, China retaliated with export controls of gallium and germanium where it is a dominant exporter to Japan and Germany, the Netherlands and the US. The overall impact of this tech rivalry has resulted in an increase of rare earth prices, disruptions in supply of chemicals and a potential reduction of 2% in global growth.14

1.3 Rising demand due to increasing digitalisation

The pandemic and emergence of new technologies increased the demand for semiconductors. The number of connected Internet of Things (IoT) devices, for example, is expected to increase 12% annually to 125 billion by 2030.15 This, in addition to increasing adoption of emerging technologies, such as AI, 5G and 6G communications as well as augmented reality technologies, is driving the need for semiconductors that could fit and power such systems.

Due to the specificities of these emerging technologies, IC design would need to produce semiconductors that are smaller, with varying voltage capacities and custom integrated functions. For example, Apple is reportedly working on a single chip that provides Wi-Fi, Bluetooth and cellular functionality for the iPhone.16 This stimulates other processes in the supply chain such as the creation of testing equipment that is up to date with current technology, appropriate verification for emerging technologies and the need to improve intellectual property protection.17

These trends present opportunities for Malaysia to grow its semiconductor industry, especially where manufacturers might require design services. Malaysia already has capabilities in Outsourcing Assembly and Testing (OSAT) and could grow capabilities in research, engineering and design that would feed into activities, such as IC design.

1.4 Shifting supply chain players

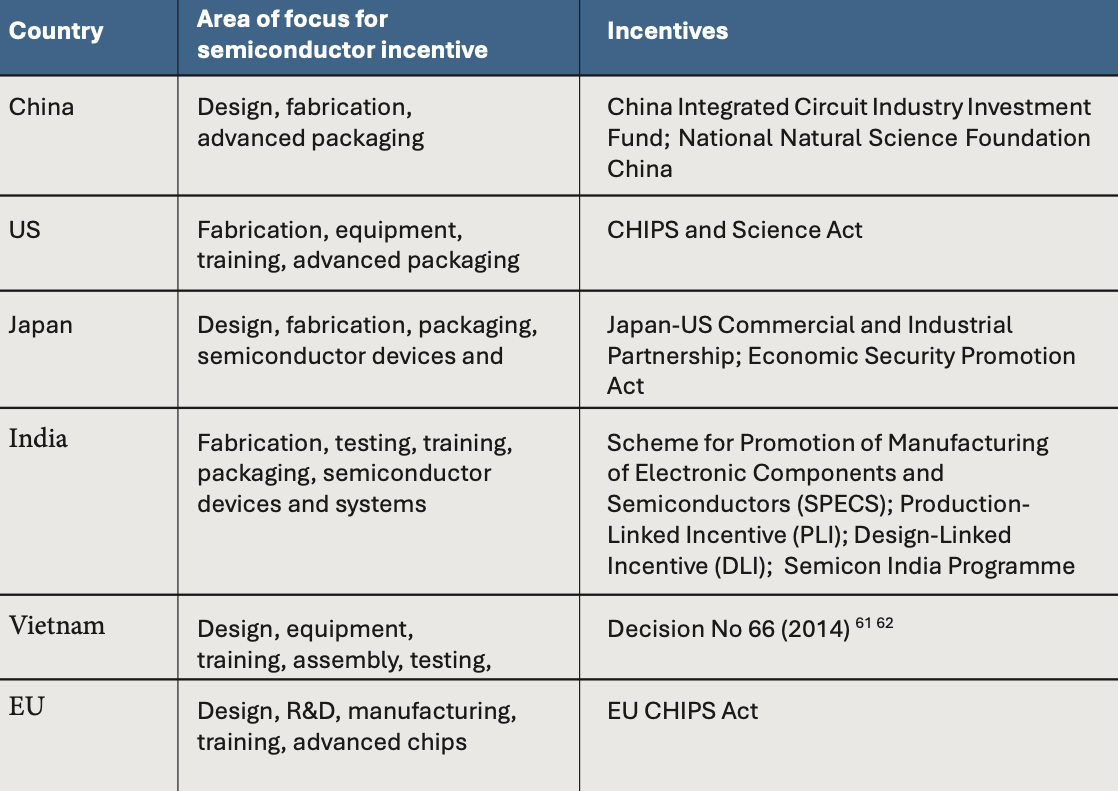

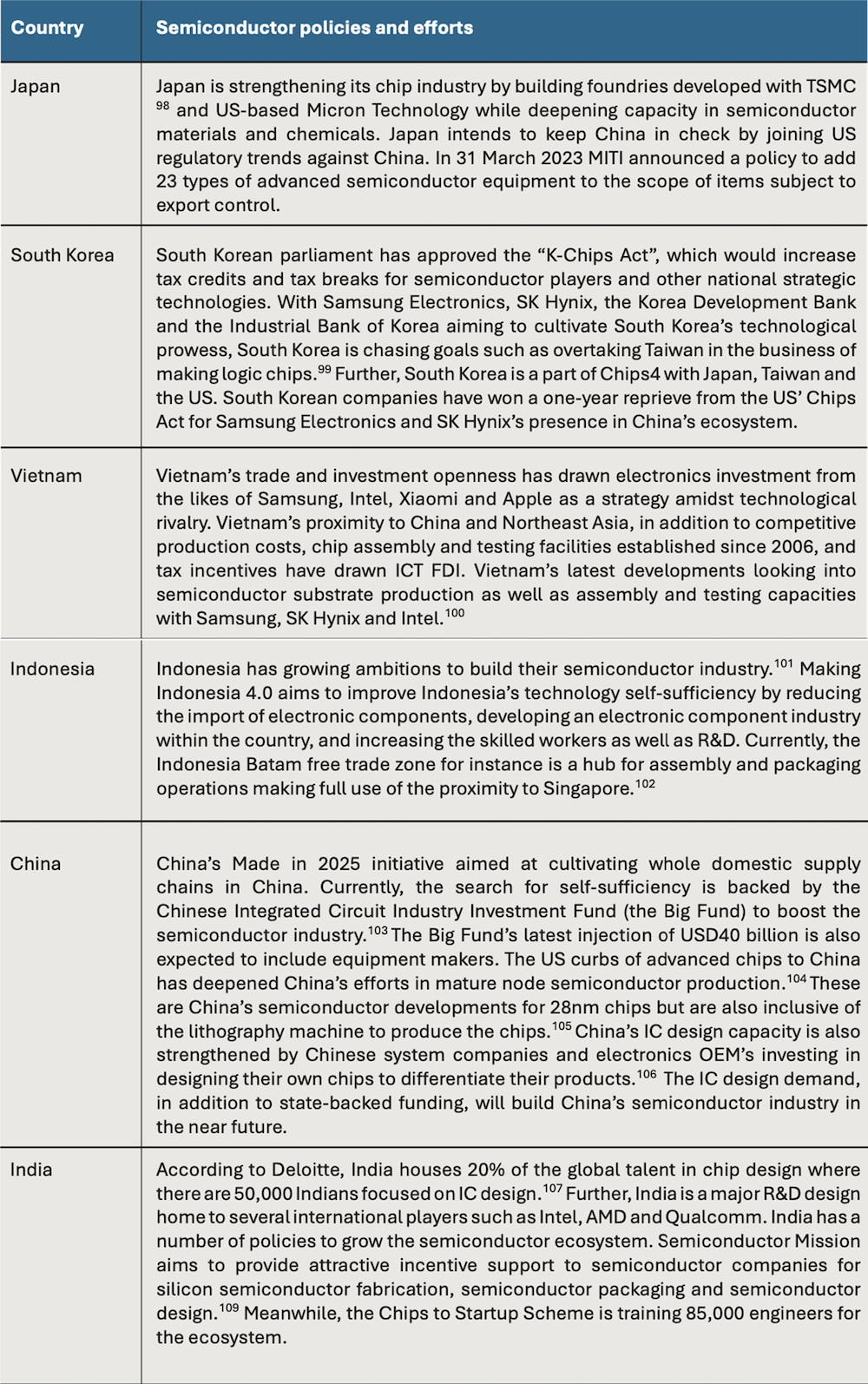

The US-China rivalry, coupled with the effects of the pandemic and various export controls, led many nations to prioritise the development of their own semiconductor manufacturing capabilities. The US-based Semiconductor Industry Association 2023 Factbook state that American-based firms have 48% of market share, followed by South Korea (19%), Japan (9%) and EU (9%), Taiwan (8%) and China (7%) 18. A CSIS report unpacks this further, articulating indispensable roles in the value chain, such as Japan providing manufacturing or wafer fab equipment and Taiwan in fabrication and chemicals19. Japan and India are among the countries introducing various incentives to build horizontal and vertical upstream capability in their semiconductor industries. In Southeast Asia, Vietnam is also aiming to build a hi-tech ecosystem.

Below are current trends in these three countries to illustrate recent developments related to semiconductors. A list of various trends in the region is in Appendix 1, which show the dynamic and competitive environment. Malaysia could learn from regional partners. For instance, Japan and India, which set specific policies on semiconductor manufacturing that is facilitated by the government. Meanwhile, Vietnam hedges technology development with high-level councils and foreign partners.

Japan

Japan is trying to reclaim leadership in the global semiconductor supply chain after decades of eroding prominence. The Ministry of Economy, Trade and Industry (METI) released a semiconductor strategy in 2020, which was later updated with more ambitious goals in 2023. It places semiconductors at the core of Japan’s economic security, to lessen its vulnerability to shocks as well as dependence on an increasingly assertive China.20 Key ambitions include producing next-generation chips.

There are two key elements to the semiconductor strategy – strengthening domestic manufacturing capability and fostering R&D for next-generation semiconductor technology through international collaboration.

In fostering R&D, a consortium of Japanese companies launched Rapidus in 2022, which aims to mass-produce 2 nano-meter advanced chips. Rapidus is in collaboration with IBM and Belgium’s IMEC. In the same year, Japan launched the Leading-edge Semiconductor Technology Centre (LSTC) as an umbrella organisation to coordinate semiconductor research, including the Rapidus workplan. LSTC is supported by existing public research organisations, such as the National Institute of Advanced Industrial Science and Technology (AIST), and will be open to researchers overseas.21

In addition, the country is encouraging greater international collaboration. Apart from Rapidus’ partnerships, TSMC has announced a new fab in Kumamoto, which is expected to spur greater investments into Japan in the next decade.

To strengthen domestic manufacturing capability, Tokyo is providing significant financial support. The government has pledged US$2.23 billion to Rapidus, is shouldering US$3.33 billion for TSMC’s Kumamoto plant, and granting Micron US$1.5 billion to expand its Hiroshima factory.22 Japan is also considering tax breaks and subsidies for companies investing in advanced semiconductors.

To summarise: to bolster its industry, Japan’s semiconductor plan outlines a strategic direction. It aims to achieve its ambitions through providing financial incentives, encouraging industrial activity and seeking international collaboration.

India

India has recognised that the key to tech self-sufficiency lies in a competitive semiconductor industry. While India has a strong information technology (IT) and software sector, its semiconductor industry is at its nascent stage, facing challenges, such as infrastructure development, talent availability and global supply chain integration. The country also faces tough competition from well-established players in East Asia, such as Taiwan, South Korea and China.

India’s intent on building a semiconductor industry is not new. It first unveiled semiconductor policies in 2007 and 2013, however, not much came to fruition due to delayed policy rollout and inadequate financial incentives.23 In December 2021, India released an updated semiconductor plan, which outlined renewed ambitions, targeted policies and financial incentives, including a US$10 billion commitment.

Some key initiatives aimed at supporting its semiconductor industry include the Scheme for Promotion of Manufacturing of Electronic Components and Semiconductors (SPECS), Production-Linked Incentive (PLI), Design-Linked Incentive (DLI) and Semicon India. To bolster capabilities, these initiatives aim to promote investments and innovation. For example, PLI has attracted US$153 billion from global and domestic companies like Samsung and Foxconn.

New Delhi is considering Assembly, Testing and Packaging (ATP) as a low-hanging fruit to gain market share in the global semiconductor supply chain.24 Advancing capabilities in ATP also help India with supply chain integration, encourage global cooperation and attract investments. This will aid in shaping an ecosystem that drives innovation and help India build a strategic foothold globally.25

India’s semiconductor plan also pushes for greater international collaboration necessary to develop a semiconductor ecosystem. The government has signed a handful of memoranda of understanding (MoU) with companies like IGSS Ventures and ISMC. The government is also facilitating Micron, which announced a new assembly and testing facility in Gujarat. The fab is expected to bring about substantial transformation for India’s semiconductor industry, i.e. attracting greater investments that could cultivate a strong semiconductor ecosystem.26

While India’s progress is promising, there are significant challenges, particularly in talent. The country holds 20% of the global talent for chip design and hosts major R&D centres for global giants, including Intel and AMD. While this indicates their huge potential for a highly skilled workforce, its ambitions towards chips manufacturing will require the government to match demand with skills. To address this, programmes aimed at developing the right talent have been rolled out. In particular, the Chips to Startup (C2S) scheme aims to train 85,000 people to provide industry-ready engineers.

India’s semiconductor road map highlights its tech ambitions and addresses existing challenges. The country has realised the importance of government facilitation in cultivating a semiconductor industry, such as implementing industrial incentives, facilitating international collaboration and providing adequate financial support. Greater government facilitation has boosted investor confidence and interest in India.

Vietnam

Vietnam’s semiconductor industry is expected to grow by around 6.7% between 2023-202827 with a goal of securing 10% of global market share of semiconductor exports.28 The country is well on its way to reach such goals. Located a mere 12-hour drive from China’s manufacturing hub, Shenzhen, Vietnam is a vibrant destination for semiconductor companies exploring a China Plus One strategy, especially arising from the US-China rivalry.29 Thus Vietnam has emerged as a vibrant investment destination for companies, such as South Korea’s Samsung and Hanmi30, even as Hanoi inks upgraded bilateral ties with the US for technology collaborations.31 As such, its role in the US supply chain has grown from previous years that in February 2023, chip imports to the US from Vietnam jumped by 75%, if compared with February 2022.32

There are several factors underpinning Vietnam’s semiconductor appeal. According to the US Geological Survey, Vietnam has the second largest rare-earth deposits, with plans to build a rare earths supply chain that could dent China’s dominance.33 Second, Vietnam’s proximity to China is a catalyst for both Chinese and other companies to flock there.34 The attraction is further supported by government incentives in the forms of tax exemptions, preferential tax rates and land rental exemption, and duty exemptions for the import of goods used to build fixed assets.35 These aim to entice companies to settle and entrench themselves in Vietnam’s industrial ecosystem.

Additionally, a working group headed by the deputy prime minister customises incentives and promotion strategies for quality, large, hi-tech and innovative projects.36 This could be inclusive of Vietnam’s first fab in semiconductors.37 These factors are further supported by competitive labour and production costs, with the promise of consistent labour supply. More than 40% of Vietnam’s graduates specialise in science and engineering38 while collaborations with industry aim to train more into the workforce to reach the target of 50,000 engineers by 2030.

Vietnam’s success can be attributed to location and the aggressive strategy to customise and secure partners to develop its hi-tech industry. Furthermore, Vietnam’s high-level council on high technology allows Hanoi to customise incentives and offer bilateral arrangements with the US and South Korea in ways beneficial to the industry.

2. Analysis

2.1 List of incentives and government assistance

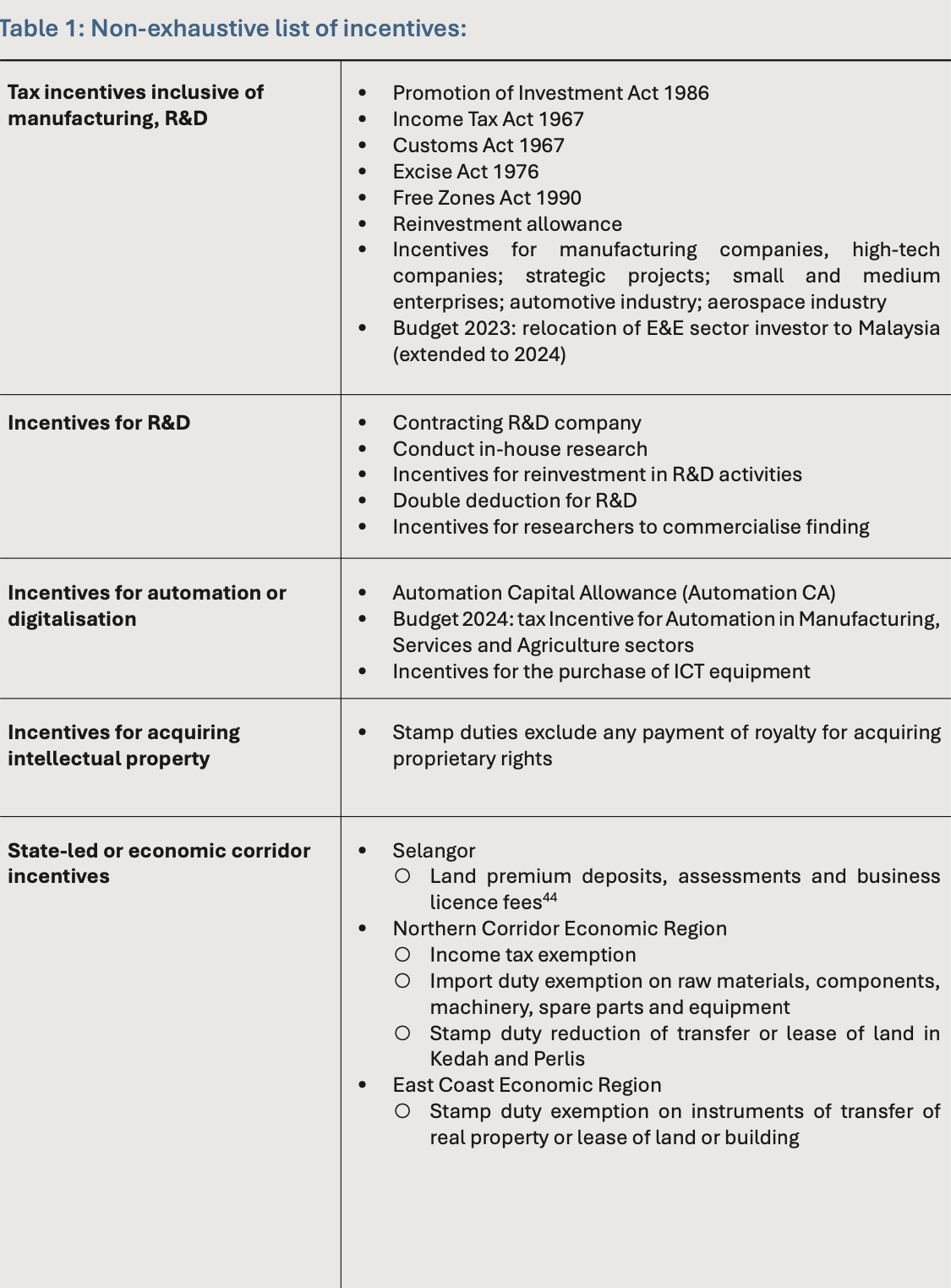

Malaysia has been offering incentives to the E&E sector since the 1970s.39 These include tax incentives to attract foreign direct investment (FDI) and grow domestic capacity, while more recently, prioritising automation. Tax and non-tax incentives, such as grants, are offered by both the federal and state governments, with Table 1 illustrating a list of non-exhaustive incentives. The incentives include exemptions of taxes from statutory income depending on the year and terms, as stated in the Promotions of Investment Act 1986. It would also include incentives for reinvestment, relocation and exports.40 Furthermore, companies conducting R&D activities are eligible for tax relief and enjoy additional benefits should they qualify for pioneer status. The NSS was allocated at least RM25 billion to operationalise the semiconductor strategies and targeted incentives, although specific details have yet to be released.

However, there are challenges to Malaysia’s incentive offerings. Despite strategic ambitions, its most recent National Industrial Master Plan stated that shortcomings of the Promotion of Investment Act as being too “sector-centric, overlapping and limiting for reinvestments”.41 In a bid to refresh the PIA, incentives would seek a mission-based approach with thematic opportunities. The task will be undertaken with a tax incentive review by the Ministry of Finance. In line with this is the establishment of a special committee on semiconductors.42 The National Semiconductor Strategic Task Force (NSSTF) with MITI as chair and the Collaborative Research in Engineering, Science and Technology (CREST), as secretariat is expected to discuss review and reforms of the incentive policy.43

2.2 Challenges with talent

According to the 2022 Malaysia Semiconductor Industry Association (MSIA) survey, the semiconductor industry needs around 13,697 factory workers and operators, 3,763 technicians, 3,411 manufacturing engineers, 2,252 design and development engineers, 1,385 office workers and 602 positions in a shared services team.45 While MSIA has also expressed that Malaysia prefers to hire locals, it has been highlighted that there is an insufficient supply of suitable or industry ready workforce.46

This can be attributed to multiple reasons. The first is the pipeline for graduates, where concerns remain over the quality of science education and language capabilities. Malaysia’s PISA ranking had taken a nosedive in 2022, with 15-year-olds scoring below the OECD average in mathematics, reading and science.47 Furthermore, while the Ministry of Science, Technology and Innovation’s Public Awareness of Science, Technology & Innovation (STI) Malaysia survey did register positive interest in STI; the interest is skewed towards health and well-being, climate change and environmental pollution.48 MASTIC’s survey illustrates trends where interest in science is lower than non-science subjects, thus impacting pathways for pupils to pursue scientific careers.

Second, Malaysia faces the challenge of brain drain and talent retention, with talents being attracted to work in other sectors and outside of Malaysia. This can be due to a few factors, including work culture that is not merit-based. Additionally, working in the E&E sector may not promise social mobility and proportionate disposable incomes, both of which are vital factors for young graduates deciding their career pathways.49 A Board of Engineers 2022 report on starting salaries stated that 35% of the electrical engineers surveyed earned less than RM2,000.50 Respondents of the survey identified causes of the low salary. Among the causes identified is an oversupply of graduates amid lack of oversight on engineering qualifications, pay grade that did not update upon completion of the training and high requirements to qualify for a higher pay scale.51 Furthermore roles in the engineering field are limited and there can be a mismatch in engineering disciplines.52

2.3 Lack of spending in R&D

Malaysia has ambitions to grow its design capabilities in the attempt to move upstream. Nonetheless, its gross domestic expenditure on research and development (GERD) has been slipping, dropping from RM17.685 billion in 2016 to RM13.483 billion in 202053 – less than 1% of GDP, and far below the government’s target of 2% GERD-to-GDP ratio set out by the National Policy on Science, Technology and Innovation (NPSTI).

Of further concern is how Malaysian businesses spend significantly lesser on R&D compared with leading countries. In 2020, businesses in Malaysia contributed a mere 34.2% towards overall GERD in stark contrast to businesses in the US, China, Japan, South Korea and Taiwan, which contributed about 70% of total GERD.54

Lastly, there are gaps in Malaysia’s commercialisation ecosystem. Malaysia’s most consistent R&D expenditure is from higher learning institutes (HLI), gross expenditure for R&D reaching RM6.37 billion in 2020, with a consistent expenditure above RM6 billion for the past decade.55 Comparatively, the business sector can be unpredictable, registering expenditure at RM10 billion in 2016 but dipping to RM4.6 billion in 2020. Meanwhile, research in government agencies increased from RM 1.147 billion in 2014 to RM2.488 billion in 2020. Against the GERD expenditures, there is a propensity to produce basic research outputs compared with experimental development, with the latter placing the output closer to commercialisation.56 Additionally, there are gaps in synergy between the academia, government and industry where basic and applied research output are not synchronised with experimental development and commercialisation goals. While Malaysia has a number of institutions dedicated to this, such as MRANTI, CREST and MIMOS, commercialisation trajectories exist in silos and do not reflect GERD activities in their R&D sectors.

This trend is exemplified in MSIA’s 2022 survey, where R&D was not captured as a top priority of semiconductor companies interviewed. Malaysia must consider harnessing R&D interest to keep its leading position in the region, especially as competing players, such as Vietnam, emerge in downstream activities.

2.4 Clarity of ease-of-doing business

Malaysia’s semiconductor industry is intertwined with global supply chains. In the 1970s, investors were drawn to Malaysia for the combination of free industrial/trade sones with reliable power supply and well- connected logistics, an English-proficient workforce, tax incentives, tariff exemptions and a relatively open regulatory environment.57 Through the years, Malaysia has built a reputation for good business ethics and transparency, along with a deep ecosystem and sub-ecosystem to cater to semiconductor investors. Furthermore, it is reputed to have an open and business-friendly environment, fair and transparent legal system with a multicultural population that could appeal to an array of investors. For example, the local Chinese population as potential partners for Taiwanese investors.

Highlighted in the NIMP are a number of agencies involved in (i) promoting and marketing opportunity, (ii) deal negotiation, (iii) investment implementation, and (iv) aftercare.58 This could mean that from deal negotiation to investment implementation, an interested investor would have to navigate various channels from investment promotion agencies, such as MIDA, to human resources guidance that includes Ministry of Home Affairs, Immigration, EPF and Socso. Furthermore, engagements are needed with state authorities and utilities at the site of business. As the semiconductor industry sharpens with competition, increasing the ease-of-doing business would enhance Malaysia’s resilience in this sector.

Additionally, communicating with the industry on developing regulations would be helpful. An example is the plans to introduce the global minimum tax of 15% on certain MNCs announced in 2022.59 With the local semiconductor industry being built on FDIs and MNC participation, the introduction of such taxes without double taxation agreements or sufficient assessment might impact on Malaysia’s appeal as an investment destination. Alternatively, Malaysia could consider other benefits to retain resilience, such as improving infrastructure or linking taxation with future industry benefits.

2.5 Shifts in supply chain players present challenges, opportunities

The geopolitical turbulence introduces specific trends in the semiconductor industry, such as the rise in homeshoring and friendshoring efforts aimed at building national capacity. This would result in a diversity of players in global value chains, which could open spaces for newer partnerships in IC design, wafer fabrication or testing.

Homeshoring and friendshoring efforts are increasing as nations eye an industry expected to hit US$1 trillion by 2030.60 Furthermore, as future technologies increase the demand for chips, a country’s own digitalisation process must consider supply chain resilience and risk in digital adoption. Malaysia’s position in the value chain would be affected by current activities other nations dedicate towards building their semiconductor industry.

In mapping incentives and investments, countries like China are investing heavily in developing self-sufficient design and fabrication capabilities while stock-piling equipment.63 64 Additionally, China takes advantage of its strong positioning in assembly, testing and packaging to devote between US$4 million and US$6.4 million to advanced packaging R&D from 2023 to 2027.65 66 The US CHIPS Act focuses on manufacturing, training and R&D.67 The CHIPS R&D funding includes measurement instruments, advanced packaging manufacturing and advanced microelectronics design and manufacturing.68

Japan is building manufacturing and packaging capacities with additional subsidies for the domestic production of semiconductor devices.69 70 The activities complement its strength in equipment and chemical manufacturing while strengthening capacities to manufacture 2nm chips. India’s efforts to boost the semiconductor industry are in fabrication, testing and packaging, as well as semiconductor devices, completing an internal value chain that is estimated to already house about 20% of the world’s semiconductor design engineers.71 72 Meanwhile, Vietnam is scaling up activities in training personnel, chip design, assembly and testing, equipment manufacturing and semiconductor devices while aiming for the first semiconductor plant.73 74 75 The EU introduced its own CHIPS Act, which aims to increase coordination and capacities in design, R&D, training as well as the manufacture and packaging of advanced chips.76 The EU aims to grow global production capacity amid a skills shortage environment.77 To that end, EU and Malaysia face a commonality of challenges in talent.

Recently, the Financial Times reported that Malaysia emerged as a surprising victor in the global semiconductor industry, where since 2022, Malaysia has seen growth of semiconductor companies in Penang – be it the expansion of existing companies, such as Intel and Infineon, or newer companies such as Fengshi.78 The growth areas are in equipment manufacturing, advanced packaging, assembly and testing, and chip production. Yet, the NIMP states ambitions to complete Malaysia’s value chain with a fabrication plant. While focus can be on building a plant, Malaysia could also explore competitive advantages that would appeal to other partners developing their semiconductor capacities.

Additionally, current trends of partnerships occur along the lines of shared values or common goals. Chips4, for instance, aims for supply chain resilience among partners.79 Supply chain resilience and innovation were also highlighted in the US-India semiconductor supply chain and innovation partnership MoU,80 Vietnam-US relationship upgrade and the Japan-India semiconductor supply chain partnership.81 As developing semiconductors utilises trade secrets and intellectual property, most collaborations are built upon and sustained on trust. Malaysia in practising active neutrality may need to project stability, transparency and security in the semiconductor sector. For the latter, providing secured physical and digital environments could be a comparative advantage.

3. Policy recommendations

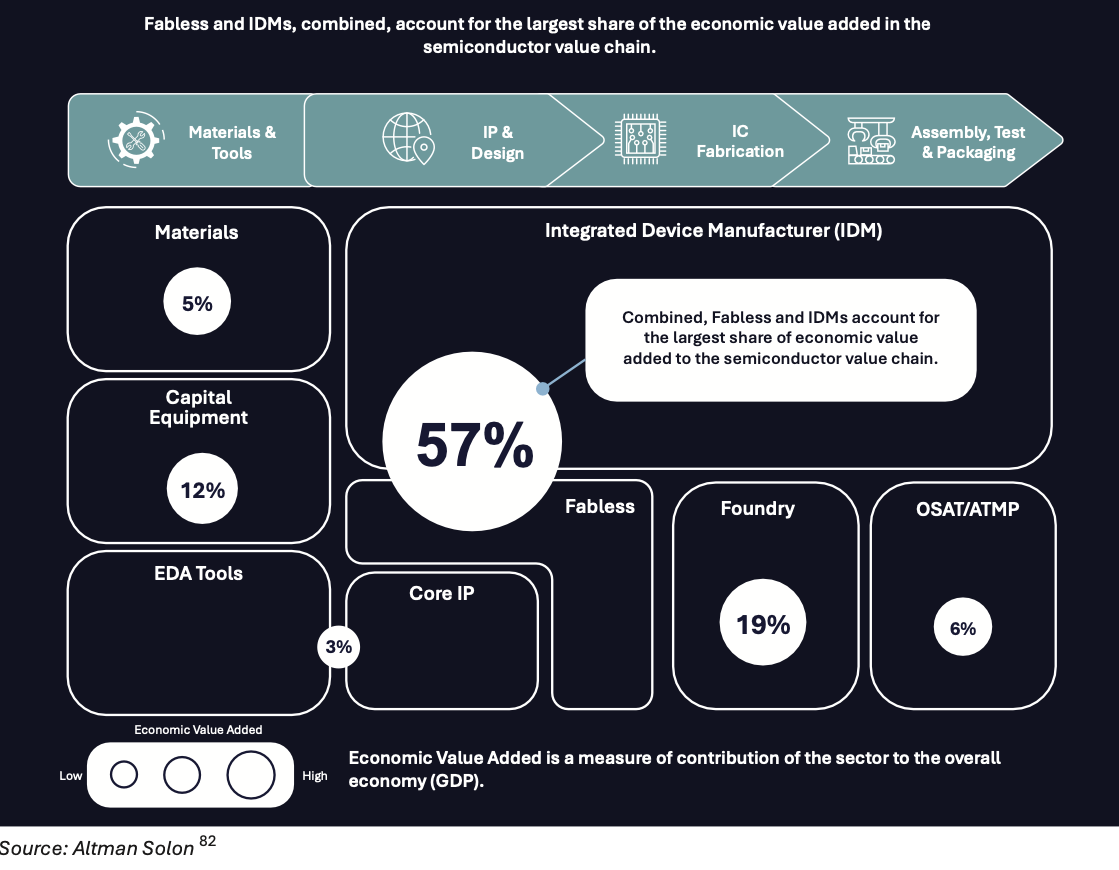

Malaysia needs to move upstream, both vertically and horizontally, to improve its global share of semiconductor exports and market share. Upstreaming vertically refers to advancing capabilities within the subset of the supply chain. For example, producing advanced packaging in the OSAT process. Upstreaming horizontally refers to moving towards the front-end of the value chain. This includes IC design and wafer fabrication.

The image above indicates the economic value of various activities in the supply chain. To note, a fabless integrated device manufacturer could unlock the largest share of economic value, at 57%, compared to OSAT, which could be limited to 6% of the value in the supply chain. This would articulate the appeal of upstreaming horizontally into activities like IC design, as articulated in the NIMP. However, increasing Malaysia’s capacity in this sector would require addressing issues, such as talent and building proficiencies for IC design. Furthermore, as Malaysia already has a 13% foothold in testing and packaging, growing this to advanced packaging would increase its participation in the global semiconductor industry.

3.1 Cultivating E&E as national pride

Malaysia’s E&E industry began in the 1970s with “eight samurais”: National Semiconductor (now Texas Instruments), Intel Malaysia, Hewlett-Packard (now Agilent), Advanced Micro Devices (AMD), Bosch, Clarion, Litronix (now Osram) and Hitachi (now Renesas).83 However, the “Silicon Valley of the East”, coined in the 1970s, has now lost its lustre. This is especially as technology further develops84 and investment in R&D necessary for innovation stayed nascent.

Addressing this requires utilising other tools, such as public messaging and branding, to woo and cultivate interest in E&E sectors. This will attract greater public support with an ensuing talent pipeline and domestic investment.

Such examples can be seen in China and Vietnam where high-tech sectors are viewed with national pride. A study of 50 CGTN videos on AI indicates deliberate messaging inciting pride, hope or fear to craft China’s narrative as a future global AI power.85 Videos on pride celebrate successes of AI adoption and communicate China’s encouraging environment to develop AI technologies. Meanwhile, Vietnam’s “Make in Vietnam” efforts in ICT cull messages to inspire the digital community to enhance its value in the global value chain.86 The messages are backed by policies and incentives that strengthen the industry, such as government investments and policy support.

Furthermore, there may be a need to cultivate global champions which can symbolise Malaysia’s achievements in the E&E sector. An example would be Proton as the national carmaker, which symbolises engineering aptitude and projections of national capacity.87 While the extent of protectionism for homegrown firms can be a concern, companies, such as Samsung and TSMC, which have made a mark in the industry did so with government support in initial stages. Today, Malaysia has significant players in the semiconductor industry, with homegrown companies, such as Silterra formed in 1995. Findings and growing these champions would promote wider interest in the industry.

3.1.1 Growing global player in thriving sector

Malaysia’s NIMP 2030 pegs the semiconductor future to three technologies: RE, EV and AI. On the latter, the field of AI is expected to be dynamic, with demand projected to reach US$207.4 billion for various chip types and functions. Nvidia, renowned graphic card maker and significant producer of AI chips, grew earnings by about 400% between 2022 and 2023.88 AI is expected to be a part of various technologies from healthcare to self-driving cars. These chips are not homogenous and efficient chip composites would need to consider the different aspects of AI necessary, such as those for training or inference to ensure maximum effectiveness.89

AI chips present opportunities for Malaysia to strengthen its semiconductor industry’s IC design capabilities, especially as there are already Malaysian companies in this space, such as Infinecs, Oppstar and SkyeChip. However, growth is impeded by challenges in building talent and capacity to boost homegrown companies.

Malaysia has a complex challenge with talent, where availability might not be the foremost problem.90 SkyeChip, one of Malaysia’s homegrown AI IC design companies, had stated luring talent to be a key component in starting operations.

This would mean attracting ICT designers with the promise of pursuing exciting cutting-edge technology, substantial pay and pride in being competitive.91 Talent pipelines can be inculcated in institutions, such as AI parks.92 Examples include Terengganu’s AI park, which interlocks university, industry and government in a triple-helix ecosystem.93 To put things in perspective, Terengganu’s AI park is focused on adoption and application of technologies, which could provide insights into IC design. Further discussions on integrating or specialising manufacturing and technology development in technology parks would have to be pursued, especially to meet NIMP goals of increasing economic complexity. Additionally, partnerships with universities94 or through training in multinational companies would be beneficial to enhance exchanges and increase capacity for innovation.95

There is also a need to complement talent development by boosting homegrown corporations in IC design and development. The IC design domain is both an entrepreneurial and an innovative role. Support for this process might require horizon-scanning exchanges, investment opportunities, access to promotional activities and targeted incentives for IC design and development. Malaysia has a few ministries and agencies tasked with the promotion of E&E players. Cultivating the semiconductor ecosystem, Malaysia needs to have a promotion strategy that streamlines approaches to elevate industry players’ opportunities and be integrated further in the international supply chain.

3.2 Promoting advanced assembly, testing and packaging capabilities as an

immediate priority

Today, Malaysia is the seventh largest semiconductor exporter with 7% of global market share. It accounts for 13% of global ATP in the semiconductor supply chain.

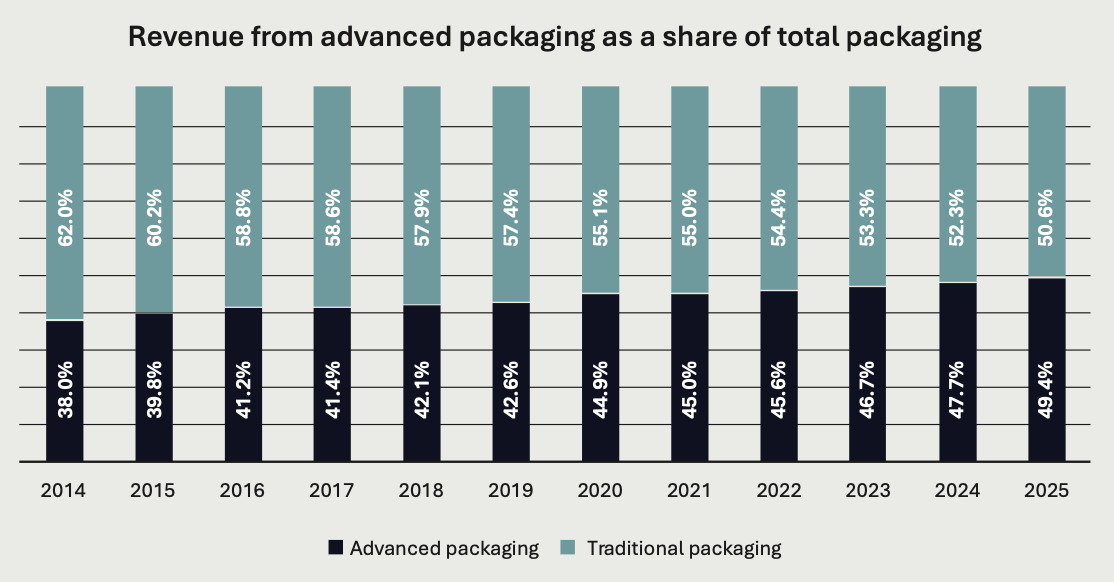

As critical technologies grow in importance, demand for higher performance chips and advanced packaging will also increase as customers seek fast and reliable computing for applications like AI. It is forecast that by 2025, demand for advanced packaging will almost equal that of traditional packaging and will likely soon exceed it (Figure 1). Malaysia’s ATP capabilities are primarily on traditional back-end packaging and would benefit from upstreaming vertically towards higher-value opportunities.

Figure 1: Advanced Packaging Market Share Evolution 2014-2025 96

There are three key reasons Malaysia should establish advanced ATP capabilities in the short term. First, as mentioned above, demand for advanced packaging is expected to increase exponentially. Not only does this help Malaysia advance the targets identified in the NIMP 2030, but it also retains and possibly expands its position in the global semiconductor supply chain.

Second, establishing advanced capabilities would make Malaysia more competitive globally. This would also attract greater investments and boost technological advancements across the semiconductor domain.

Third, advanced ATP capabilities are difficult to replicate. For example, India is trying to establish a foothold in the ATP market as a low-hanging fruit but is at least a decade away from attaining high-end capacities. Malaysia should capitalise on its existing market presence, enhance its capabilities and synergies with the demands of the global tech market. This can ensure that Malaysia is indispensable to the global semiconductor supply chain.

Currently, there are some advanced packaging capabilities being developed in Malaysia, such as through ASE Technology and Intel. Further targeted incentives are required, specifically for players to tap into capital and training necessary for upstreaming on this front. The government should facilitate greater investments to help gain momentum developing advanced ATP capacities.

Moreover, there is interest within Malaysia’s semiconductor industry to move towards advanced packaging. Nonetheless, there may be concerns over the geopolitical risk arising out of the US-China tech rivalry, which would necessitate a coordinated response from MITI and MOFA to mitigate the risks to the semiconductor industry.

3.3 Developing design capabilities

Malaysia is experienced in competing on price but not capabilities. On the latter, the country must invest in developing design capabilities.

Research is considered beneficial for companies to identify new market opportunities, understand customers’ need and develop new technologies. However, invigorating research, design and engineering requires a comprehensive strategy for technology transfer and public-private partnerships. An example of public-private partnerships for research is Taiwan’s Industrial Technology Research Institute (ITRI). ITRI’s history with ICs includes setting up public-private partnership councils, facilitating external technical advisory committee, which could facilitate technology-transfer agreements, providing training opportunities for technicians and pursuing partnerships with universities to develop emerging technologies. ITRI is the SME answer to external research and design houses, where its business model is shaped by serving as a design house for a network of small and medium industry players.

Such ideas are present in grooming small medium enterprises to fit in larger manufacturing ecosystem, such as the Penang Automation Cluster in Batu Kwan Industrial Park.97 However, the cluster and park are focused on manufacturing with lesser emphasis on building R&D, innovation and business synergy. In upstreaming horizontally, Malaysia should grow talent in IC design, which may require exploring knowledge-transfer, training and wage policies that could appeal to MNCs and universities. Malaysia also needs to consider investing in the capacity in existing facilities while enhancing its successes.

4. Conclusion

Malaysia could play a critical role in international semiconductor production. Malaysia’s talent pool, language proficiency, access to infrastructure and deep-rooted semiconductor ecosystem mean that it has the components to grow the industry further.

A targeted strategy that encompasses concrete milestones, talent pipelines, incentives and investments is necessary to chart the way forward. This paper also proposes focusing on moving upstream vertically by building advanced packaging capabilities. The advanced packaging capabilities could be complemented by talent development and design incubation. The paper proposes moving upstream horizontally in the future. Malaysia could scale up support for homegrown companies in IC design, which could demonstrate the capabilities in this field. Lastly, this paper recommends looking into building messaging for the E&E sector as national pride to restore interest in engineering and sciences. This could be a part of a long-term strategy to retain talent in the sector.

5. Glossary

| ATP | Assembly, Testing and Packaging refers to the semiconductor production that involves the assembly of the chips, testing for its functionality and packaging into its protective cases. |

| CHIPS4 | Chip alliance consisting of US, Japan, Taiwan and South Korea. The alliance is also known as Fab4 |

| DLI | India’s Design Linked Incentive for semiconductors |

| EDA | Electronic design automation |

| GERD | Gross Domestic Expenditure on Research and Development |

| IC | Integrated circuits are used interchangeably with semiconductors and can also be known as chips, microchips or microelectronics. The integrated circuit is a wafer that could have thousands of resistors, capacitors and diodes. |

| IDM | Integrated Device Manufacturer oversees all processes in the production of semiconductors from planning to producing the semiconductor. Examples of IDMs are the likes of Samsung and Intel. |

| IOT | Internet of Things |

| ITRI | Industrial Technology Research Institute |

| LSTC | Japan’s Leading-edge Semiconductor Technology Center in charge of coordinating Japan’s semiconductor research, inclusive of the Rapidus workplan. |

| NIMP | The New Industrial Master Plan announced by the Ministry of Investment, Trade and Industry in 2023 |

| OSAT | Outsourced Assembly and Testing are vendors providing packaging and testing services |

| PLI | India’s Production Linked Incentive related to semiconductors |

| SPECS | India’s Scheme for Promotion of Manufacturing of Electronic Components and Semiconductors |

| TSMC | Taiwan Semiconductor Manufacturing Company |

5. Appendix

Appendix 1 – Overview of targeted policies and efforts for the semiconductor

industry in selected countries

Endnotes

- Malaysia Productivity Corporation. (2022). Subsector Productivity Report: Electrical and Electronics.

- Department of Statistics Malaysia. (2024). National Account: Gross Domestic Product.

- Ministry of Investment, Trade and Industry. (2023). Malaysia External Trade Statistics: Trade Performance for Year 2023 and December 2023. MATRADE.

- Malaysia External Trade Development Corporation. (2023). MATRADE Promotes Malaysia as a Global Leader in E&E. Semicon SEA.

- Deloitte. (February 2023). MSIA 2022 E&E Survey. MSIA.

- Teng, L. J. (18 November, 2021). Cover Story: Why companies are flocking to Batu Kawan Industrial Park. The Edge Weekly.

- Ministry of Investment, Trade and Industry. (2023). New Industrial Master Plan 2030.

- Dermawan, A. (2023). DPM: Malaysia aims to achieve 15pc market share in global semiconductor industry by 2030. News Straits Times.

- Wayland, M. (2021). Chip shortage expected to cost auto industry $110 billion in revenue in 2021. CNBC.

- Solomon, F. (2021). Covid-19 surge in Malaysia Threatens to Prolong Global Chip Shortage. Wall Street Journal.

- Reuters. (2023, October 24). ”Nvidia says U.S. speeded up new export curbs on AI chips”. Reuters.

- Ajao, E. (2022). Nvidia now needs special license to export AI chips to China. TechTarget.

- Koc, C., & Leonard, J. (2023, January 27). Biden wins deal on Netherlands, Japan on China chip export limit. Bloomberg.

- Lv, A., & Goh, B. (2023, July 4). Beijing jabs in US-China tech fight with chip material export curbs. Reuters.

- IHS Markid. (n.d.). Number of connected IoT devices will surge to 125 billion by 2030. Semiconductor Digest.

- Elevate Semiconductor. (2023). Acind the Test: The Chips Behind the Chips. Engineering.

- Bailey, B. (2023). What does 2023 have in store for chip design?. Semiconductor Engineering.

- Semiconductor Industry Association. (n.d.). 2023 Factbook.

- Thadani, A., & Allen, G. C. (2023, May 30). Mapping the Semiconductor Supply Chain: The Critical Role of the Indo-Pacific Region. Center for Strategic and International Studies.

- Ministry of Economy, Trade and Industry Japan. (2023, June 6). Press Conference by Minister Nishimura [Speech].

- Shivakumar, S., Wessner, C., & Howell, T. (2023). Japan Seeks to Revitalise its Semiconductor Industry. Center for Strategic and International Studies. Retrieved from CSIS:

- Mochizuki, T. (2023). Japan prepares $13 billion to support country’s chip sector. Bloomberg.

- Bhandari, K. (2023). Is India ’ready’ for semiconductor manufacturing. Carnegie India.

- Thomas, P. (2023). India set to challenge China’s dominance in semiconductor packaging. Networkworld.

- Tripathi, N. (2023). Can India Truly Become a global semiconductor hub?. Forbes India.

- Zeeb, A. (2023). Decoding India’s Ambitious Leap Into Semiconductor Manufacturing. Inc 42.

- Viet Nam News (2023, Dec 11). Make-in-Viet Nam movement key to digital transformation and semiconductor growth.

- ARC Group. (2023). Vietnam Holds Promise as a Global Semiconductor Hub.

- Le, P., & Nguyen H. T. (2022). Vietnam climbs the chip value chain. East Asia Forum.

- Nguyen, T. (2023). Vietnam attracts giant investments in semiconductor industry. The Investor.

- Kurlantzick, J., & McGowan, A. (2023). Assessing the Bolstered US-Vietnam Relationship. Council of Foreign Relations.

- Quy, L. (2023). Vietnam’s path to multibillion-dollar semiconductor industry. VNExpress.

- Guarascio, F., & Vu, K. (2023). Inside Vietnam’s plans to dent China’s rare earths dominance. Reuters.

- Nguyen, H. (2023). Vietnam’s wary of China’s ’Swift, Large-scale’ Investment. VOA.

- Dezan Shira and Associates. (2021). Vietnam Unveils New Criteria for Hi-Tech Enterprises: Decision 10. Vietnam Briefing

- Huong, G. (2021). Special working group set up to facilitate investment projects. Socialist Republic of Vietnam Government News.

- Guarascio, F. (2023). Vietnam eyes first semiconductor plant, US officials warn of high cost. Reuters.

- ARC Group. (2023). Vietnam Holds Promise as a Global Semiconductor Hub.

- Malaysian Investment Development Authority. (n.d.). Chapter 2: Incentives for New Investments.

- PwC. (n.d.). Malaysia Corporate – Tax credits and incentives.