Jaideep Singh was quoted in The Edge Malaysia Weekly on 25 March 2026

by Adam Aziz

This article first appeared in The Edge Malaysia Weekly on March 16, 2026 – March 22, 2026

THE conflict in the Middle East has triggered concerns about fuel prices and supply just as Malaysians begin the festive season of Hari Raya Aidilfitri. The oil market went from an oversupply position to a shortage overnight after Tehran declared that it would attack any oil tankers crossing the Strait of Hormuz, through which about 20% of the world’s energy supply passes.

Prime Minister Datuk Seri Anwar Ibrahim addressed the fuel supply concerns last Wednesday, assuring that the nation had enough secured until May. The following day, in an attempt to further calm the public, national oil company Petroliam Nasional Bhd (PETRONAS) pointed out that mitigation measures were in place to support supply continuity from June onwards.

The benchmark Brent crude oil has surged more than 30% to about US$100 per barrel.

While Anwar said the subsidised RON95 petrol would be capped for the foreseeable future at RM1.99 a litre, the pump price of unsubsidised petrol has risen 68 sen to RM3.27 a litre. Subsidised diesel is maintained at RM1.88 a litre in Peninsular Malaysia and RM2.15 in Sabah and Sarawak, but unsubsidised diesel is up 29% to RM3.92 from RM3.04. The price of the premium RON97 petrol has spiked 22% to RM3.85 a litre from RM3.15.

Higher crude oil prices would lift the government’s fuel subsidy bill to RM3.2 billion a month, from RM700 million before the conflict, according to Minister of Finance II Datuk Seri Amir Hamzah Azizan.

The Ministry of Economy, in a brief reply to The Edge says, “The government is closely tracking both inventories and supply flows, while coordinating with key industry stakeholders to ensure readiness under various scenarios. At this stage, there is no indication of immediate stress on domestic fuel availability.”

Being an oil and gas producer with domestic refining capacity, Malaysia does not have to press the panic button yet as it is in a better position than most of its Asean peers. But things could get difficult if the war continues beyond a couple of months and crude oil prices rise further.

Meanwhile, the Iran war has put a spotlight on the nature of the country’s fuel supply reserves and its reliance on imports of crude petroleum and condensates — two-thirds of which come from the Middle East — for domestic use.

The Edge explores Malaysia’s current fuel supply situation, how the issue is being addressed and what could be in store for the nation.

From the ground to the pump

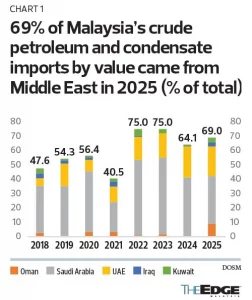

In 2025, Malaysia imported RM54.11 billion worth of crude petroleum and condensates, 69% of which came from the Middle East (see Chart 1). This compares with the RM23.76 billion worth of exports last year, most of which went to Thailand (26.1%), Australia (25.7%) and Japan (15.8%).

Malaysia imports both crude oil as well as processed products. The reason it imports crude oil is economic: oil extracted from the country’s seabed, such as the Tapis crude from Peninsular Malaysia and Kimanis crude from Sabah, is of a higher grade as it is less viscous and has a lower sulphur content (meaning cleaner) than that from other places. Thus, it requires less refinery processing to produce higher-value products such as jet fuel and can command a higher price tag in the market.

To maximise the economic benefits, Malaysia exports most of the oil it produces. Refiners here blend some of it with cheaper, higher-sulphur oil imports, like those from the Middle East, to be processed into downstream products such as fuel for cars. (Malaysia has been importing Middle East oil since the 1970s.)

The feedstock imported into Malaysia is processed by refineries owned by players such as PETRONAS, Hengyuan Refining Co Bhd (KL:HENGYUAN), Petron Malaysia Refining & Marketing Bhd (KL:PETRONM) and Dutch firm Vitol. PETRONAS’ refining capacity is parked under PETRONAS Chemicals Group Bhd (KL:PCHEM) and some of the products are marketed domestically by PETRONAS Dagangan Bhd (KL:PETDAG).

At the next stage, the finished products are transported to storage terminals nationwide, including for commercial customers such as airlines and ships at nearby storage facilities. They are also eventually transported to petrol stations — Petron and PETRONAS to their own outlets, Hengyuan to Shell stations and Vitol to BHPetrol stations.

Part of our domestic refining capacity produces products that can be further processed into higher-value petrochemicals that ultimately leave the country. As such, Malaysia also imports refined products (largely from Singapore, South Korea and China) to fill product-specific deficits (particularly diesel and jet fuel), says Rystad Energy oil analyst Nithin Prakash.

The bulk of imports “ultimately supports transport demand, including road transport, aviation and marine fuels”, Nithin tells The Edge. “Based on Malaysia’s oil demand structure, transport fuels (gasoline, diesel, jet fuel) account for roughly 70% of the total refined product consumption.”

Reserve levels vary

Despite being an oil and gas producer, Malaysia “does not maintain a formal strategic petroleum reserve in the traditional sense”, says Nithin. Neither is the country a member of the International Energy Agency (IEA), which requires members to hold at least 90 days of emergency stockholding, a requirement applied to Organisation for Economic Co-operation and Development countries.

To manage short-term supply disruptions, Malaysia relies on commercial inventories, domestic refining capacity and regional trading flexibility, says Nithin. The stockpiles are stored across government and commercial storage facilities held by PETRONAS, refiners and oil marketing companies, he adds.

Based on industry estimates and policy statements, Malaysia has one to two months of refined product stocks. This compares with IEA member countries Japan (with strategic reserves of more than eight months) and South Korea (seven months) and its association countries such as China (just under three months), Indonesia (23 days) and Thailand (three months), while Singapore, like Malaysia, relies primarily on commercial storage.

Companies typically maintain commercial storage as part of their corporate strategies. Tank terminal operator Dialog Group Bhd (KL:DIALOG), for instance, operates 5.14 million cu m of capacity, 50.8% of which is used for independent or short-term clients, while the balance is dedicated to long-term clients.

However, maintaining large stockpiles is costly. According to data from the Ministry of Economy sighted by The Edge, declining domestic production and reliance on imported crude make it challenging for Malaysia to maintain larger strategic reserves.

Further downstream, at the fuel trader or retailer level, inventory typically lasts about two months in normal times, in line with storage capacity, an industry source explains.

In a March 9 report, BIMB Securities points to Hengyuan’s crude oil storage capacity of “roughly two weeks”. As for airports, fuel storage facilities will typically hold four to seven days of supply, it adds.

Petrol stations can store about three days of supply, according to Ministry of Economy data.

Getting alternative sources

The conflict in the Middle East has already prompted changes across the supply chain. According to an industry source in the fuel retailer sector, some suppliers have shortened supply commitments to two months from the usual six months since the war began.

PETRONAS has also redirected Malaysian crude oil to domestic refineries to maximise fuel production for local consumption. Historically, part of the country’s crude oil production has been sold through spot tenders apart from long-term contracts. Industry estimates suggest that roughly 20% of Malaysian crude is sold on the spot market.

“Yes, technically this is feasible. Crude oil produced from our Malaysian assets, such as the Labuan Crude Oil Terminal (LCOT) is acceptable to Malaysian refineries,” says independent oil producer Hibiscus Petroleum Bhd (KL:HIBISCS) in a brief reply to The Edge.

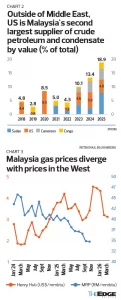

Meanwhile, PETRONAS has secured additional sources of crude oil supply from West Africa and Latin America to reduce dependence on any single shipping route. Over 22% of Malaysia’s imports in 2025 came from these regions (see Chart 2).

At the same time, the national oil company is preparing its refinery in Pengerang — operated by Pengerang Refining Co Sdn Bhd and Pengerang Petrochemical Sdn Bhd (PRefChem) — to help balance gasoline and jet fuel demand as crude oil feedstock becomes available.

PRefChem — a joint venture between PETRONAS and Saudi Aramco — receives crude oil feedstock from the Saudi oil company, although it is unclear where the JV ranks on Aramco’s priority list for deliveries during a supply disruption.

There is hope that Saudi crude could eventually make its way to customers, including Malaysia, which gets 33% of its total imports from the largest Gulf state. The country “does have the option of rerouting supplies to the Red Sea via overland pipelines”, says Institute of Strategic and International Studies (ISIS) Malaysia analyst Jaideep Singh, although just slightly more than half of the pipelines’ seven million barrels per day capacity is operating effectively.

Malaysia could also “adjust supply management to safeguard domestic fuel availability if needed”, says MARC Ratings Bhd chief economist Dr Ray Choy.

Globally, IEA members have agreed to release 400 million barrels, or 30% of their collective reserves, which could cover 20 days of shortage from the Strait of Hormuz, back-of-the-envelope calculations show.

“The strategic importance of oil supply creates a strong alignment of incentives among major geopolitical actors, making coordinated action more likely should the oil supply situation worsen,” says Choy.

Gas supply safe, but price risk looms

The conflict in the Middle East has also threatened natural gas flows from Qatar, the world’s largest liquefied natural gas (LNG) exporter.

From a supply perspective, Malaysia’s exposure appears limited. Most of the gas supplied to consumers and power plants in the peninsula are sourced from domestic offshore fields, with the balance imported from Australia, according to data from the Department of Statistics Malaysia.

Although PETRONAS signed an agreement with QatarEnergy earlier this year to import LNG from the Gulf state, industry sources say shipments have yet to begin.

The Qatar shortage “has sent LNG prices skyrocketing in Europe and East Asia”, says ISIS’ Jaideep. A prolonged shutdown of Qatari production “could test Taiwanese and South Korean resilience, and by extension, Malaysia’s chip testing activities”, even though alternative sourcing is in the works, he adds.

Oil price increases would benefit PETRONAS as a major global gas exporter and trader. The Malaysia Reference Price, which tracks the country’s gas export prices, has declined since last year (see Chart 3) and could rebound as a result.

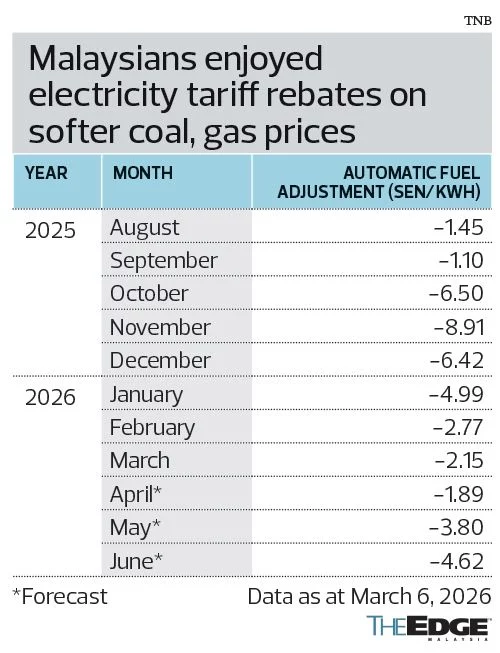

Gas is a major fuel source for Malaysia’s power plants, meaning rising prices could erode the energy tariff rebate known as the Automatic Fuel Adjustment that non-residential electricity users have enjoyed since August last year. As it is, the spot price of coal, another key fuel source for power generation, has already jumped above US$130 per tonne, exceeding the electricity tariff benchmark of US$97.

Energy security back in focus

For Malaysia, the issue is “more about the price” rather than supply, says an executive at an oil company with Malaysian operations, considering that 80% of the global oil and gas supply does not pass through the Strait of Hormuz and remains available to the market.

Using Malaysian crude is more expensive, as stated earlier. And as supply shrinks, pump prices will go up as fuel retailers are forced to bid higher to secure supply.

However, another executive is less sanguine about supply security because if the Strait of Hormuz remains closed for the next few months, “everyone will be 20% short of their normal consumption”.

At press time, the global community is receiving mixed signals on the continued restrictions in the Strait of Hormuz. Amid reports of Iran “cooperating” with certain countries seeking safe passage, the number of vessels passing through daily remains in the single digit from more than 100 before the conflict.

“Malaysia is not the only one who will be short of oil as its regional peers’ stockpiles also face depletion, Wood Mackenzie research director Yaw Yan Chong tells The Edge. “If the whole world is short, what alternative can there be?”

He warns that in a worst-case scenario, “prolonged supply uncertainty could trigger export restrictions by major regional product exporters — including India, China and South Korea — if crude flows from the Middle East Gulf are significantly curtailed”.

Analysts and economists say the government can, legally and institutionally, direct PETRONAS to prioritise domestic supply over export contracts, although they opine that it is unlikely to fully curb exports unless the crisis escalates, especially considering the risk to its reputation as a reliable energy partner, which is a cornerstone of its commercial standing.

One mitigating factor “lies in Malaysia’s upstream energy sector”, says MARC’s Choy. “Given that the baseline infrastructure and institutional capacity to strengthen Malaysia’s position in global energy supply chains already exists, the Iran war may serve as a catalyst accelerating industry development.”

Another takeaway is that Malaysia “is better positioned than pure importers like Singapore or the Philippines, but it has underinvested in formal strategic reserves and remains exposed to price shocks on the large share of refined products it imports from the Gulf”, says Rystad’s Nishin.

The country can and likely should “build a formal strategic petroleum reserve, something Malaysia has long discussed but never implemented. The current crisis makes it urgent,” he adds.

This article was first published in The Edge Malaysia Weekly, 25 March 2026